10 Steps to Improving Your Credit Score

03/04/2022

Your credit score plays an important role in many aspects of your life, from the rate you get on a car loan to passing a background check for your dream job. In lots of little ways, having bad credit can keep you from achieving your short- and long-term plans. Luckily, improving your credit score isn't a mystery; it is a simple process that you just need to follow consistently.

Step 1: Check your credit score

You cannot begin to make changes to your credit score if you don't know what your credit score is. Makes sense, right? So wha tis it and where do you get your hands on it?

Your credit score is determined based on your credit history. Actions like your payment history, types of credit, and amount of credit are reported and recorded. Positive behavior, like making on-time payments, improves your credit score. Negative information, like late payments or bankruptcies, hurt your credit.

Your credit score is a number between 300 and 850 and is built looking at the last seven years of history. The lower the number, the poorer the credit.

The first step to fixing your credit is to know exactly where you stand. Too many people know they have "bad credit," but don't know exactly what their credit score is or what negative marks are on their credit report. Every American is entitled to a free copy of their credit report from all three major credit bureaus. You can request your free credit reports here.

Step 2: Clear any mistakes

Now that you have your credit report, look through it to see what is negatively impacting your credit score (also called a derogatory mark). They could be things like late payments, an account in collections, or defaulting on a loan. Some of these might be legitimate, and we will discuss how to deal with those in a moment, but right now we are looking for anything that might be a mistake.

If you find an error, you will need to send a letter to the creditor (whatever company claims you owe them money) letting them know of the mistake. The Federal Trade Commission (FTC) provides a free letter template for filing this dispute.

There are other companies, like Credit Karma, that provide digital tools to help you identify and dispute errors on your report.

Step 3: Settle what you can

Once we have cleared all the errors from your report, you should focus on resolving what you can that is your legitimate debt. There is a technique called "pay for delete." Essentially, you call the collection agency holding the debt and ask them to remove the derogatory mark once you settle the debt. Not all agencies will do this as the legality of doing so is somewhat questionable.

Regardless of if you choose to try and negotiate a "pay for delete" deal, you should try and settle whatever debts you can, as that will always help your credit score.

Step 4: Prioritize card repayment

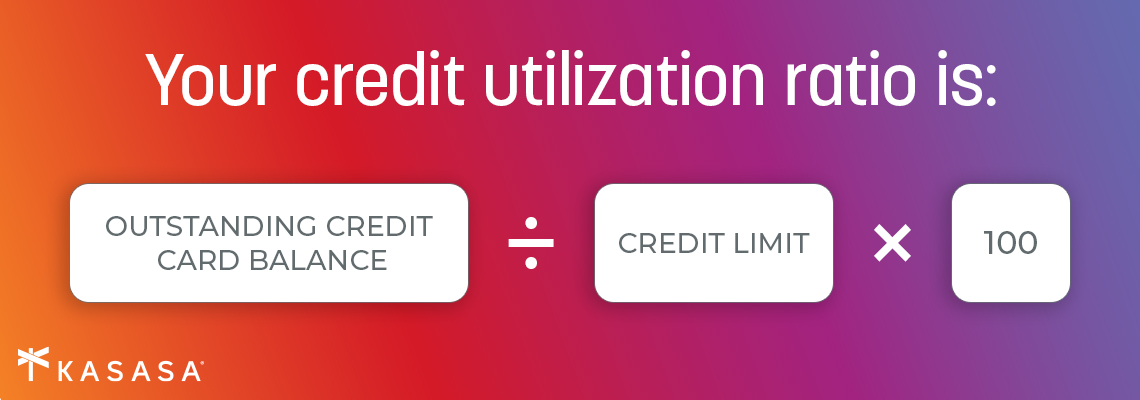

One of the factors considered in your credit score is something called "credit utilization." It is the amount of credit you have used in relation to your total combined credit limit. For the sake of simple math, pretend you have a credit line of $1,000. You spend $500 of it. You have utilized 50% of your credit ($500/$1000).

A general rule of thumb is to try to keep your credit utilization under 30%. The lower, the better, as it is a proxy of how well you are handling your debt.

To help improve your credit score, if you have more than one credit card, look for the account with the highest utilization score (one that is close to being maxed out) and pay that down. A card with a $100 limit and $99 spent will have a credit utilization of 99%. A card with a $1,000 limit and $90 spend will have a credit utilization of 9%. In this step, you're looking for cheap and quick fix. This is different from a strategy to get out of debt; if that is your goal, or the balances are similar, target the credit account with the highest interest rate.

Step 5: Automate bill payment

The single best thing you can do for your credit is to pay bills on time, consistently, and in full. Sometimes we fail to pay on time, even when we could, simply because we're human and we forget. Remove the option to forget and enroll in automatic payments.

Bill pay is so valuable to the companies waiting to get your payment that many institutions will charge a fee for individual payments. Check with each insurance provider, cell phone carrier, and financial institution to see what benefits there might be to setting up a recurring payment.

Step 6: Keep accounts open

Another heavily weighted variable in your credit score is the length of an account. Some people will advise cancelling your credit card when it gets paid off in order to remove temptation. If you feel like you need that, then certainly do it, however you will be removing an old line of credit. Consider cutting up the card but keeping the account open. If you are still tempted, contact the credit card company and ask them to reduce your credit limit.

Step 7: Automate credit building

Remember, credit is built by successfully paying off debts on time. A simple way to ensure that it happens is to put small, recurring payments on a card and then have it automatically paid off in full each month. For example, put your water bill on automatic pay. Have that be the only bill on this credit card and set the card up to be paid in full every month.

Step 8: Get rent payments counted

Not all bills are reported. For example, your rent payments don't help you build credit, even though that is likely your most expensive monthly bill. There are some reporting services out there that will help make sure you rent helps to build your credit.

These services work by either contacting your landlord, or by serving as a middle-man in making your rent payments (you cut them a check, then they pay your landlord). You'll probably have to pay a monthly fee for this service, but it could be worth it for the boost in your credit score.

Step 9: Consider additional products

Another product you might want to consider enrolling in is Experian's Boost. This feature helps you to get credit for your phone and utility bills. Be sure to read the terms and conditions of any program offering to help you improve your credit. Know the costs, length of commitment, and benefits before enrolling.

Step 10: Don't open new accounts

There are two issues to be aware of when it comes to opening new accounts.

First, applying for the account usually requires a credit inquiry. There are two types of credit checks hard and soft pulls. Soft pulls are often done for things like a background check and don't impact your credit score. Hard pulls are done when you apply for a line of credit (like a car loan) and they do lower your credit score anywhere from 5 to 20 points.

Second, opening several new accounts rapidly shows that you are looking to get a lot of credit, which can be interpreted as having financial difficulties. Waive off those impressions by only opening new credit accounts when it will benefit you in the long run.

Fixing your credit score isn't hard, but it does require you to follow some basic rules and stick with them: know your scores, pay on time and in full, get credit for everything, and then continue credit monitoring. Repeating these steps raise your credit, maybe not immediately, but successfully.

As always, FCCU has staff to help you with credit questions. Contact your local branch for help!

Article Source: Kasasa